Energy Efficiency with Demand Response: Can a Single Business Model Solve Both Problems?

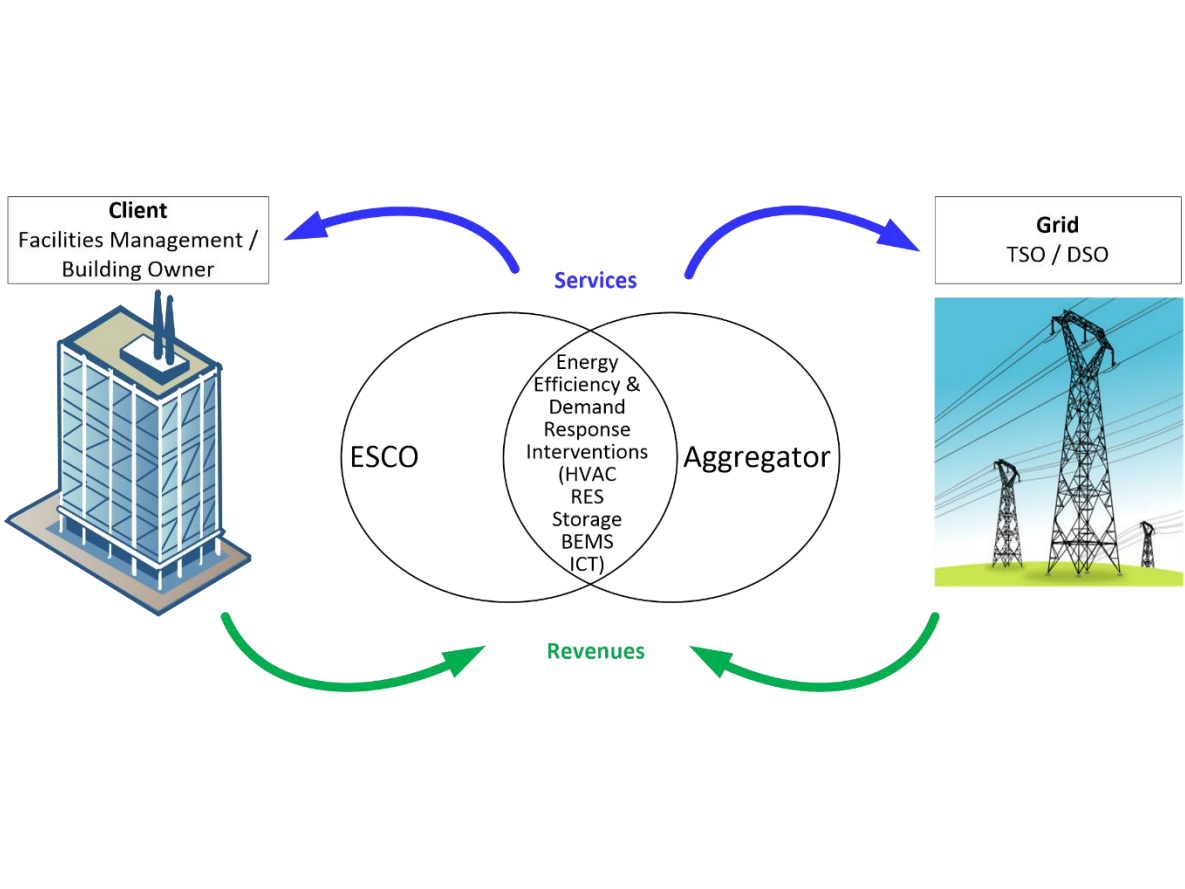

A few months ago we talked about the regulations and market conditions that exist across Europe that promote or restrict the viability of this ‘joint energy services’ business model. Recently we have taken this research a step further and looked at the business case for implementing this model in various countries by using a tried and tested assessment tool, the SWOT analysis. This is a good starting point for drafting a detailed strategy for the combined ESCO (energy saving) and Aggregators (demand response) business model. To augment this classic tool, we considered each category from the point of view of each of the stakeholders in the value chain, in this case the ESCO, Aggregator, Financier, Client and Facilities Management companies. What we achieved was a far more detailed picture of the potential for joint energy services offered under an Energy Performance Contract (EPC) than a traditional SWOT could hope to give. For each country, the SWOT analysis answers the following questions: • What are the strengths and weaknesses of the joint energy services business model for each stakeholder in the context of each country’s market? • What opportunities and threats does the market in each country present to each stakeholder involved in operating a joint energy services business model? By taking this approach we learned that there is currently no single European country that presents the optimum conditions for joint energy services. In many ways this isn’t really a surprise – if the perfect market conditions already existed then ESCOs and Aggregators would already be working together, and our research wouldn’t be needed. However, our analysis did highlight some of the key policies, regulations and market forces that are most likely to facilitate the growth of this business model, such as: • A strong and well-established ESCO market that is trusted by their clients. • Government support for implementing EPCs helps them to gain traction in the market. • Several demand-side response markets that are open to aggregation. • Regulations on demand response programme participation is not overly bureaucratic. • Political commitment to energy efficiency and renewable energy targets. Of all the countries assessed, the ones that are most suited to the joint energy services EPC are the UK and France, closely followed by Ireland. The UK and France both have well developed ESCO markets, several DSR markets that are open to participation and a TSO that is open to adjusting the regulations to encourage more participation in flexibility markets. Both markets still have barriers to overcome, however, there are no regulations that would prevent the delivery of a joint services business model if clients could be persuaded to accept it. In Ireland, whilst the ESCO market is still small, this is largely due to the lack of awareness of the benefits of EPC among clients rather than any regulatory barriers. The Irish TSO has opened several DSR markets and is hampered mainly by large minimum load requirements and the need to bid into the market annually. Despite this, it would be possible to operate a joint services EPC in Ireland if clients could be persuaded to participate. The countries least suited to implementing a joint energy services EPC are currently Italy, where aggregation of loads to participate in the DSR markets is not yet legally allowed, and Denmark, where the large proportion of hydro-electric power stations on the grid and excess capacity on the network means there is a weak business case for demand response services. This is just a snapshot of our findings. If you’re interested in a more detailed breakdown of the SWOT analysis by country, you can download our full report from http://novice-project.eu/resources/(opens in new window) We’ll also be publishing a selection of the SWOT tables in our next blog post, so keep an eye out for that!

Countries

France, Ireland, United Kingdom